{kind=link}

Money New Year’s Resolutions: Top 7 Smart Tips 2024

Money new year’s resolutions offer a unique opportunity to turn a fresh page and start building a more secure financial future. For many, setting clear financial goals—like saving more, paying off debt, or sticking to a budget—can transform the year into one of prosperity and peace of mind. Here’s a quick guide to get you started:

- Create a realistic budget – Know your income and expenses.

- Set clear saving goals – Aim for short-term and long-term goals.

- Manage debt wisely – Pay off high-interest debts first.

- Protect your finances with insurance – Shield against unexpected events.

As the new year unfolds, real change doesn’t happen overnight. The “Fresh Start Effect,” as highlighted by Katy Milkman, reminds us that there are countless opportunities throughout the year to recommit to our goals. This mindset lets us see each new day as a chance to improve our financial habits and outcomes.

My name is Amanda Schmitt, and I’ve dedicated years to helping families find practical solutions to everyday challenges. With my background in occupational therapy and my experience running Life As Mama, I’ve learned how to simplify complex tasks, making concepts like money new year’s resolutions accessible and achievable for everyone.

Money new year’s resolutions terms to learn:

– new year resolutions for men

– new year resolution thoughts

– new year’s day 2025 resolution

Money New Year’s Resolutions

When it comes to money new year’s resolutions, think of them as your roadmap to financial well-being. Tackling areas like budgeting, saving, debt management, and credit scores can set you up for a prosperous year ahead. Let’s break it down:

Budgeting

Creating a budget is your first step. It’s like a financial GPS, guiding you toward your goals. Start by tracking your spending to see where your money goes. Use online budgeting tools to make this easy. Identify your fixed expenses like rent and utilities, and set aside money for savings. A clear budget helps you prioritize needs over wants.

Saving

Setting saving goals can be empowering. Whether you’re saving for a vacation, a new car, or retirement, having specific targets keeps you motivated. For a balanced approach, consider the 50/30/20 rule: allocate 50% of your income to necessities, 30% to discretionary spending, and 20% to savings. This ensures you’re meeting your needs while also planning for the future.

Debt Management

Debt can feel like a heavy weight. But with a plan, you can lighten the load. Focus first on high-interest debts, like credit cards. The debt avalanche method—paying off the highest interest rate debt first—can save you money in the long run. Alternatively, the debt snowball method—tackling the smallest debts first—can provide quick wins and keep you motivated.

Emergency Fund

Life is unpredictable. That’s why an emergency fund is crucial. Aim to save three to six months’ worth of living expenses. This fund acts as a financial cushion, covering unexpected costs like medical bills or car repairs. Having this safety net in place can significantly reduce stress and help you handle emergencies without resorting to credit.

Credit Score

Your credit score is your financial report card. A good score can save you money on loans and insurance. To improve your score, pay bills on time, reduce debt, and avoid opening too many new accounts at once. Regularly check your credit report for errors, and dispute any inaccuracies you find.

By focusing on these areas, you’re not just making resolutions; you’re laying the groundwork for a healthier financial future. Small, consistent actions can lead to big changes over time. Stay committed to your goals, and revisit them regularly to track your progress. Each step you take brings you closer to financial freedom.

Create a Budget and Stick to It

Creating a budget is like setting the foundation for your financial house. It helps you understand where your money goes and ensures you have enough for the essentials and future savings. Here’s how to get started:

Track Your Spending

The first step in budgeting is to track your spending. This means keeping an eye on every dollar that leaves your wallet. Start by listing all your expenses for a month. This will give you a clear picture of your spending habits and highlight areas where you can cut back.

Use Online Budgeting Tools

Technology can be your best friend when it comes to budgeting. There are many online budgeting tools and apps that can help you organize your finances. These tools categorize your expenses, track your income, and even alert you when you’re overspending. They make budgeting less of a chore and more of a habit.

Identify Fixed Expenses

Next, focus on your fixed expenses. These are the regular bills you can’t avoid, like rent, utilities, and insurance. Knowing these costs helps you determine how much money you have left for other things. Once you have your fixed expenses noted, you can plan around them, ensuring they’re always covered.

Set Savings Goals

With a clear picture of your spending and fixed expenses, it’s time to set savings goals. Whether it’s for a rainy day, a dream vacation, or retirement, having specific goals keeps you motivated. Start small if you need to, and gradually increase your savings. Remember the 50/30/20 rule: allocate 50% of your income to necessities, 30% to wants, and 20% to savings.

By implementing these strategies, you’ll not only create a budget but also stick to it. A budget isn’t about restricting your spending but rather about making sure your money works for you. Keep revisiting and adjusting your budget as needed to stay on track toward your financial goals.

Build and Maintain an Emergency Fund

Life is full of surprises, and not all of them are pleasant. Unexpected expenses like car repairs, medical bills, or even losing a job can throw a wrench in your financial plans. This is where an emergency fund comes in. It’s your financial safety net, providing peace of mind and stability when life gets unpredictable.

Why You Need an Emergency Fund

Imagine your car breaks down unexpectedly. Without an emergency fund, you might have to rely on credit cards or loans, which can lead to debt. An emergency fund helps you cover such expenses without derailing your budget or going into debt.

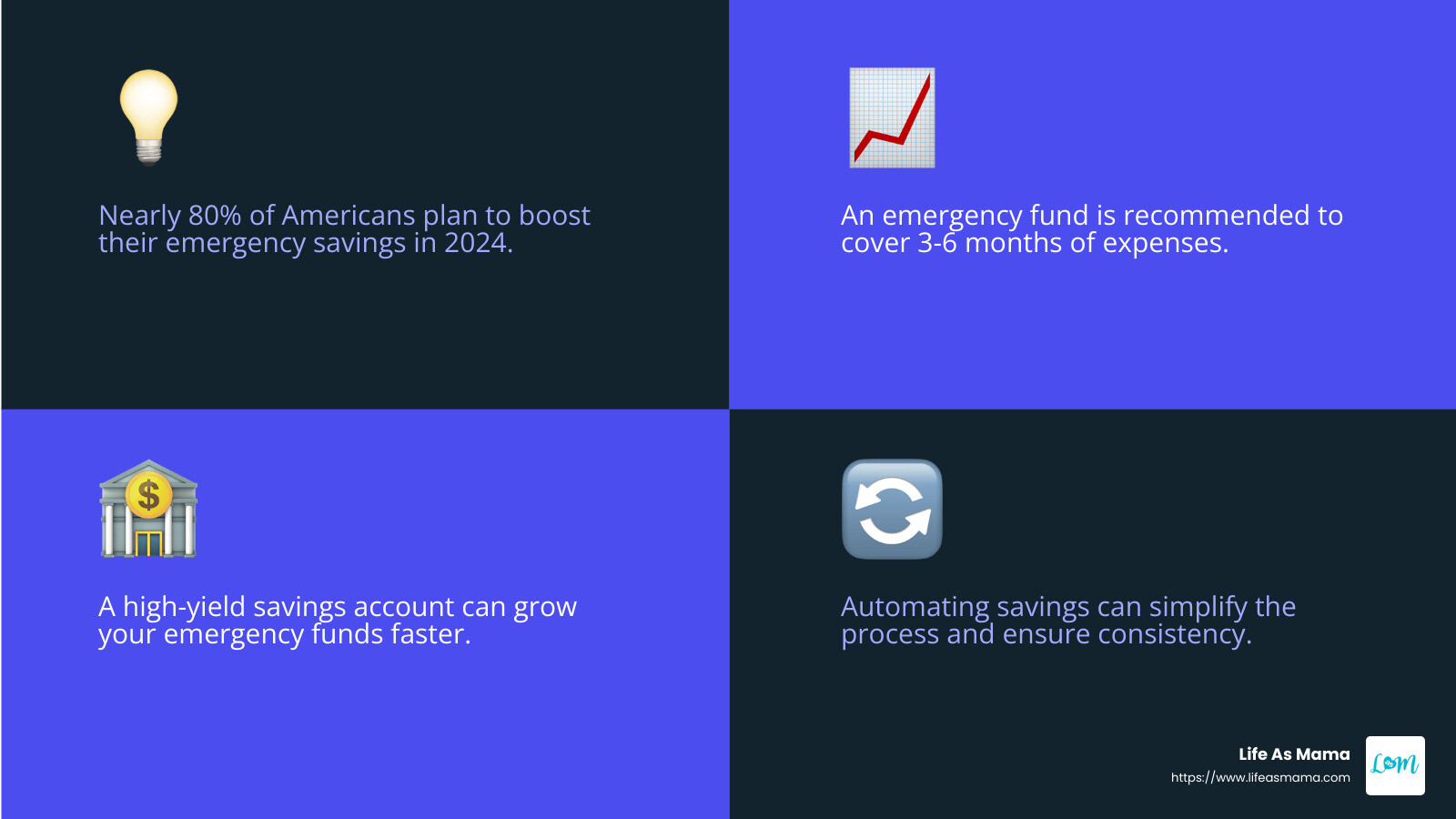

According to experts, it’s wise to have three-to-six months’ worth of living expenses saved up. This might seem daunting, but the key is to start small and build gradually.

Where to Keep Your Emergency Fund

A savings account is a great place to store your emergency fund. It’s easily accessible, and some accounts offer interest, so your money can grow over time. Just ensure it’s separate from your regular spending account to avoid the temptation of dipping into it for non-emergencies.

Consider using a money market fund or certificate of deposit (CD) for potentially higher interest rates. These options can help your savings grow faster than a standard savings account, but be mindful of any restrictions on withdrawals.

Building Your Emergency Fund

Start by setting a small initial goal, like $1,000. Once you’ve reached that milestone, aim to save one month’s worth of expenses, then two, and so on. This step-by-step approach makes the task less overwhelming and more achievable.

You can automate your savings by setting up a monthly transfer from your checking account to your emergency fund. This way, you consistently contribute without having to think about it.

The Benefits of Financial Security

Having an emergency fund not only shields you from financial stress but also gives you more control over your life. It allows you to make decisions based on what’s best for you, rather than being forced into choices due to financial constraints.

With a solid emergency fund, you’re better prepared for whatever life throws your way. It’s a crucial step in achieving financial security and independence, allowing you to focus on your long-term goals with confidence.

By building and maintaining an emergency fund, you’re taking a proactive step toward safeguarding your financial future. This preparation ensures that unexpected expenses don’t derail your progress, keeping you on track toward a prosperous financial journey.

Manage and Reduce Debt

Debt can feel like a heavy backpack, slowing you down on your financial journey. But with a plan, you can lighten the load and move forward. Here’s how to tackle credit card debt, create repayment plans, and consider debt consolidation.

Tackling Credit Card Debt

Credit card debt is like a sneaky thief that steals your money through high interest rates. To fight back, start by paying more than the minimum each month. Even a small extra payment can make a big difference over time.

Consider the avalanche method: pay off cards with the highest interest rates first. This saves you money on interest. Or try the snowball method: pay off the smallest debts first to gain momentum and motivation.

Creating Repayment Plans

A clear repayment plan is your roadmap to debt freedom. Start by listing all your debts, including amounts, interest rates, and minimum payments.

Set a realistic monthly payment goal. Make sure it’s an amount you can stick to without neglecting other financial needs. Use a budgeting tool to track your progress and adjust as needed.

Considering Debt Consolidation

Debt consolidation means combining multiple debts into one, often with a lower interest rate. This can simplify payments and save money.

You might use a personal loan or a balance transfer credit card for consolidation. Just be aware of any fees or terms that could affect your savings.

Debt consolidation isn’t a magic fix. It requires discipline to avoid racking up more debt. But with focus and commitment, it can be a powerful tool in your debt-reduction arsenal.

By managing and reducing debt, you’re freeing up resources for savings and investments. This not only improves your financial health but also brings peace of mind, allowing you to focus on building a brighter financial future.

Optimize Your Investment Portfolio

When it comes to growing your wealth, optimizing your investment portfolio is key. Let’s explore asset allocation, diversification, and risk tolerance, which are crucial for your financial success.

Asset Allocation: The Right Mix

Asset allocation is like the recipe for a successful portfolio. It’s about spreading your money across different types of investments—like stocks, bonds, and cash. This mix should match your goals, risk tolerance, and how long you plan to invest.

Why is it important? Imagine your portfolio as a pie. If one slice (like stocks) is too big, a downturn could really hurt. But if you balance it with bonds and cash, you can weather storms better.

Diversification: Don’t Put All Eggs in One Basket

Diversification is about owning a variety of investments within each asset class. Think of it like having different flavors of ice cream. If one melts, you still have others to enjoy.

How to diversify? Mutual funds and ETFs are great tools. They let you own a basket of stocks or bonds, reducing risk without needing to buy each one separately.

Risk Tolerance: Know Your Limits

Risk tolerance is your ability to handle ups and downs in the market. Some people can ride the roller coaster of stock prices, while others prefer a smoother ride.

Find your comfort zone. If market swings make you anxious, lean more towards bonds and cash. If you’re okay with volatility for higher returns, stocks might be your thing.

Regular Monitoring and Rebalancing

Once you’ve set your asset allocation and diversified, don’t just sit back. Markets change, and your portfolio can drift from your original plan. Check in at least twice a year and rebalance if needed.

Rebalancing means adjusting your investments back to your target allocation. For example, if stocks have grown too much, sell some and buy more bonds to keep your balance.

By optimizing your investment portfolio, you’re setting the stage for financial growth and security. This thoughtful approach not only helps you achieve your money new year’s resolutions but also ensures you’re prepared for whatever the market throws your way.

Protect Your Financial Future

Securing your financial future isn’t just about growing your wealth; it’s about protecting what you have. Here’s how insurance coverage, estate planning, and beneficiary updates play a vital role in this process.

Insurance Coverage: Guarding Against the Unexpected

Insurance is like a safety net, catching you when life throws a curveball. Whether it’s health, life, or disability insurance, having the right coverage can save you from financial disaster.

- Health Insurance: Protects against large medical expenses. Consider a plan that fits your medical needs and budget. A high-deductible plan might be a good choice if you’re generally healthy.

- Life Insurance: Essential if you have dependents. Group term life insurance through your employer can be a cost-effective starting point. If you have significant liabilities, consider additional coverage.

- Disability Insurance: Safeguards your earning power. A 20-year-old has a 25% chance of becoming disabled before retirement, so this coverage is crucial.

Estate Planning: Your Legacy Matters

Estate planning isn’t just for the wealthy. It’s about making sure your wishes are honored and your loved ones are cared for.

- Write a Will: This ensures your assets are distributed according to your wishes, avoiding the lengthy probate process. It’s not just about money; it can also detail who will care for your dependents.

- Revocable Living Trust: Useful for large or complex estates, it allows you to specify how assets are managed and distributed. Consult an estate attorney to see if this is right for you.

- Durable Powers of Attorney: Appoint trusted individuals to make decisions on your behalf if you’re incapacitated. This can include financial and healthcare decisions.

Beneficiary Updates: Keep Information Current

Regularly updating your beneficiary information is a simple yet crucial step in financial planning.

- Why Update?: Life changes, like marriage or a new child, may require updates. Even if beneficiaries haven’t changed, ensure their contact details are current.

- Where to Update?: Review beneficiaries on retirement accounts, insurance policies, and bank accounts. These designations can override what’s in your will.

Taking these steps helps protect your financial future and gives you peace of mind. By addressing these areas, you’re on your way to achieving your money new year’s resolutions and ensuring a secure future for you and your loved ones.

Next, we’ll tackle some of the most frequently asked questions about money resolutions, helping you start the new year on the right financial foot.

Frequently Asked Questions about Money New Year’s Resolutions

What are common financial resolutions?

At the start of a new year, many people focus on improving their financial health. Common financial resolutions include:

- Budgeting: Creating and sticking to a budget helps you track spending and prioritize savings. It’s a key step in managing your finances effectively.

- Debt Reduction: Paying off high-interest debt, like credit card balances, can save money and reduce financial stress. Consider setting up a repayment plan or exploring debt consolidation options.

- Savings: Building an emergency fund and saving for specific goals, like a vacation or new car, are popular resolutions. Aim to save at least 20% of your income each month if possible.

How can I start the new year off right financially?

Starting the year on a strong financial footing involves setting financial goals and establishing a money routine. Here’s how:

- Set Clear Goals: Define what you want to achieve financially. Whether it’s increasing your savings or buying a home, having clear goals can guide your financial decisions.

- Establish a Routine: Regularly review your finances. This could be a weekly check-in with your budget or a monthly review of your investment portfolio.

- Adopt a Positive Mindset: Stay optimistic and focused on your financial goals. This mindset can help you overcome challenges and stay motivated throughout the year.

How to set intentions for money?

Setting intentions for money involves aligning your financial habits with your long-term goals. Consider these steps:

- Identify Priorities: Determine what matters most to you financially. This could be saving for retirement, paying off debt, or preparing for inflation concerns.

- Be Mindful of Interest Rates: With interest rates affecting loans and savings, understanding their impact can help you make informed decisions. For example, higher rates might encourage you to pay off debt faster or look for better savings accounts.

- Stay Flexible: Financial circumstances can change, so be prepared to adjust your plans as needed. Regularly reassessing your goals ensures they remain relevant and achievable.

By addressing these frequently asked questions, you can set a solid foundation for your money new year’s resolutions and work towards a more prosperous and secure financial future.

Conclusion

At Life As Mama, we believe in empowering families with practical, family-friendly financial tips. Our goal is to help you steer the complexities of personal finance with ease and confidence. Whether you’re creating a budget, building an emergency fund, or planning for your financial future, our guides are designed to be straightforward and actionable.

Family-friendly financial tips are about making money management accessible to everyone in the household. By involving the whole family in financial discussions, you can instill healthy money habits in children and ensure everyone’s on the same page. This collaborative approach not only strengthens family bonds but also sets a strong foundation for future financial success.

Our practical guides are crafted to simplify complex financial concepts. From understanding the ins and outs of debt management to optimizing your investment portfolio, we break down each topic into easy-to-follow steps. We aim to make financial literacy attainable for all, offering strategies that fit seamlessly into your day-to-day life.

As you start on your journey to financial well-being, small, consistent efforts can lead to significant progress. Accept the new year as an opportunity to set and achieve money new year’s resolutions that align with your family’s goals and aspirations.

For more insights and tips on making this year your best yet, visit our 10 Ways to Make 2022 Your Best Year Yet page and explore a wealth of resources custom to your needs.

Let’s make this year a financially prosperous one, together!

Related Images:

Amanda Schmitt

Latest posts by Amanda Schmitt (see all)

- Fruit Infused Waters That Make Summer Hydration Fun - July 1, 2025

- Light Up Your Life: Home Lighting Decoration Ideas - June 30, 2025

- Let’s Taco Party! Easy Steps for a Perfect Taco Bar Setup - June 27, 2025